This week - Erdogan keeps throne, Greece rating upgrade, Iran vs the Taliban, Tunisian hydrogen, and new 'Central Banks' section.

Week of May 29th, 2023.

This week we are focusing on elections in Greece and Turkey. Erdogan is winning once again, as he has dominated Turkish politics since 2003. His neighbouring prime minister in Greece is not happy with his victory, so a second vote will take place on the 25th. We are also taking a look at border clashes between Iran and Afghanistan, which seem to be escalating quickly.

New section: Central banks

Starting this week, we will maintain a section on central banks and monetary policy in emerging and frontier markets. From the bottom of the newsletter, we will monitor 30 economies in Eastern Europe, Africa, Latin America and Asia. We will analyse significant developments and keep you up to date with monetary policy schedules.

Turkey election update

President Recep Tayyip Erdogan gets to keep his throne at last, with 52% in the second round. Election runoffs were scheduled to be held on Sunday the 28th of May after neither side was able to reach the 50% threshold. Erdogan was facing his biggest challenge yet as the Turkish opposition rallied support for Kemal Kilicdaroglu, an economist and leader of the Republican People’s Party who received a total of 44.8% while his opponent fell just short of a majority at 49.5%. Closing polls indicate that Erdogan is narrowly leading his opponent but note that anything could happen.

New support for Erdogan

Last week, Sinan Ogan another candidate and leader of the right-wing nationalist alliance ATA who came in third with around 5% of votes endorsed Erdogan, further harming the chances of an opposition victory and granting Erdogan at least five more years as president.

Greece elections to repeat on June 25th

While the focus is on Erdogan’s re-election, its neighbour Greece is also seeing two votes. On May 21st general elections gave a victory to Prime Minister Kyriakos Mitsotakis, from the New Democracy party, with 40% of the vote. Hoping to gain an absolute majority in parliament, Mitsotakis has called for a re-run on June 25th. The left opposition is deeply split between Syriza (20%), which governed through the worst of the crisis, the old social-democratic party PASOK (11%), and the Communist Party (7%).

Credit rating upgrade - at what cost?

On the eve of the first vote, the Financial Times ran a piece on a remarkable achievement for an emerging Greece. The rating agency Standard & Poor could soon be upgrading the grade of Greek debt into BBB-, the lowest threshold to count as “investment grade”, moving up from the “junk” category. This comes as S&P improved its outlook for the country from stable to positive. This will mean much lower borrowing costs for the heavily indebted nation, a welcome sign of progress. For the FT, the headline was “greatest turnaround”. Two days later, however, the Editorial ran a piece highlighting the many troubles and challenges still facing Greece.

Taken as a whole, the Greek population is poorer than it was before the crisis, lagging behind most of the EU. Average Greek wages are down more than 25% in real terms since 2008. GDP in real terms is down 20%. Exports increased, although this was due to domestic demand being crushed and wages falling. Greek products were therefore cheaper abroad, while locals were buying less. Productivity, or production for that matter, did not increase. Nonetheless, cheaper borrowing costs grant a new opportunity to the country. After more than a decade of austerity, the new question will be where the new Mitsotakis government chooses to invest.

Africa Development Bank board members meet

The annual meeting of the boards of governors of the African Development Bank Group took place between 22-26 May 2023 in Sharm El Sheikh, Egypt. The meetings were stated to focus primarily on mobilizing the private sector for climate and green growth in Africa. Climate policy in Africa has been a complicated issue over the years as much of the continent still relies heavily on non-renewable energy with a limited number of countries mobilising and willing to invest in green energy. Other important factors include political crises and a lack of resources to efficiently alter their energy policies.

Climate risks spur action

The increasingly visible impacts of climate change have spurred many leaders to consider giving more efforts to develop their green energy initiatives and move away from their dependence on fossil fuels. This year many African countries are experiencing higher levels of droughts and food shortages with East Africa being the region most affected. By encouraging greater participation from the private sector in developing green energy, the bank argues that this could lead to more sustainable growth for the entire continent in the long term and build stronger economies capable of competing more equitably with other regions of the world.

Fighting on Iran-Afghanistan border

There are reports of fighting near Hirmand, on the border between Iran and Afghanistan. This would be the second time since 2021, although videos of troop movements indicate fighting is escalating. Both sides seem poised to intimidate the other; Taliban commander Abdel Hamid Khorazani has boasted his troops are ready and he can “take Tehran in 24 hours”.

War for water

Fighting likely arose from a dispute over water supply. Afghanistan dominates most of the water of Hirmand River, which provides water to Eastern Iran’s agriculture, at a time when the latter country is traversing a severe drought. Tehran claims that the Taliban are not fulfilling their quotas as agreed back in 1973. On the other hand, Afghanistan is enduring economic collapse due to sanctions and financial isolation, ever since the Taliban takeover. The war-torn country’s GDP fell by 21% and there is a famine underway. Kabul is demanding larger payments for the supply of water, while Tehran has rejected this outright.

Another point of tension could be the trade of Afghan-produced drugs, such as hash and opium. The Taliban and other armed groups profit extensively from this sector, which flourished during the war. Routes towards Europe, the main buyer, traverse Iran, whose anti-smuggling efforts attack the Taliban’s revenues, especially in the context of the economic crisis.

Currently, the main bargaining chip that the Taliban can use is their military; they took over $5bn worth of US and their allies’ equipment, during their haste withdrawal, including 167 aircraft, 3,000 armoured vehicles, and 358,000 rifles. Likewise, they could support separatist armed groups in Iranian Baluchistan. Analysts believe the Taliban could be trying to bring in foreign mediators to achieve a favourable deal. China could have an interest in negotiations, as it is heavily invested in Iran, while it is attempting to bring stability into Central Asia. China analyst Moritz Rudolf argues that the economic value of Iran is much greater than Afghanistan’s as a partner, but security concerns over the latter are remarkable.

Tunisia green hydrogen initiative

Tunisia prepares to export over 5 tonnes of green hydrogen to Europe by 2050 under an initiative that has been in the works since 2022. This is according to the General Director of the Electricity and Energy Transition at the Ministry of Industry, Belhassen Chiboub. If successful, this strategy may improve the country’s standing as an energy hub for Europe due to its already advantageous location and bordering both Algeria and Libya.

Gas pipeline

The Trans-Mediterranean pipeline was completed in 1983 and was constructed to transport Algerian natural gas to Italy via Tunisia. Serving as an important distribution point of natural gas into Europe particularly after sanctions placed on Russian gas following the war in Ukraine. Energy experts are hoping the same could be achieved for a cleaner energy fuel as research efforts are ongoing.

Commitment to green energy

Chiboub has also affirmed that Tunisia must follow the examples of other countries and transition to renewable energy sources. This objective may prove to be challenging, especially concerning the ongoing political and economic crises placing strain on the country's ability to invest and carry out its global commitment to fighting climate change.

Central Banks

This week, we will be hearing from the Bank of Thailand, which is due to make an announcement on Wednesday 31st. With falling inflation, the expectation is that rates will be kept low for the time being, they stand at 1.75%. East Asia in general is experiencing much lower inflation than much of the world. In developed markets, Latin America, and Africa, inflation and high rates are common phenomena. Next week, we will see announcements from the Reserve Bank of India and the Bank of Russia. Later in the month, we also expect the Latin American heavyweights Brazil, Mexico, and Chile alongside Turkey. After losing hope in an Erdogan loss, traders and investors are already preparing for Turkey to run out of foreign exchange reserves. Both the monetary policy announcement on June 22nd and the result of Turkey’s presidential election – favouring the incumbent – will be key.

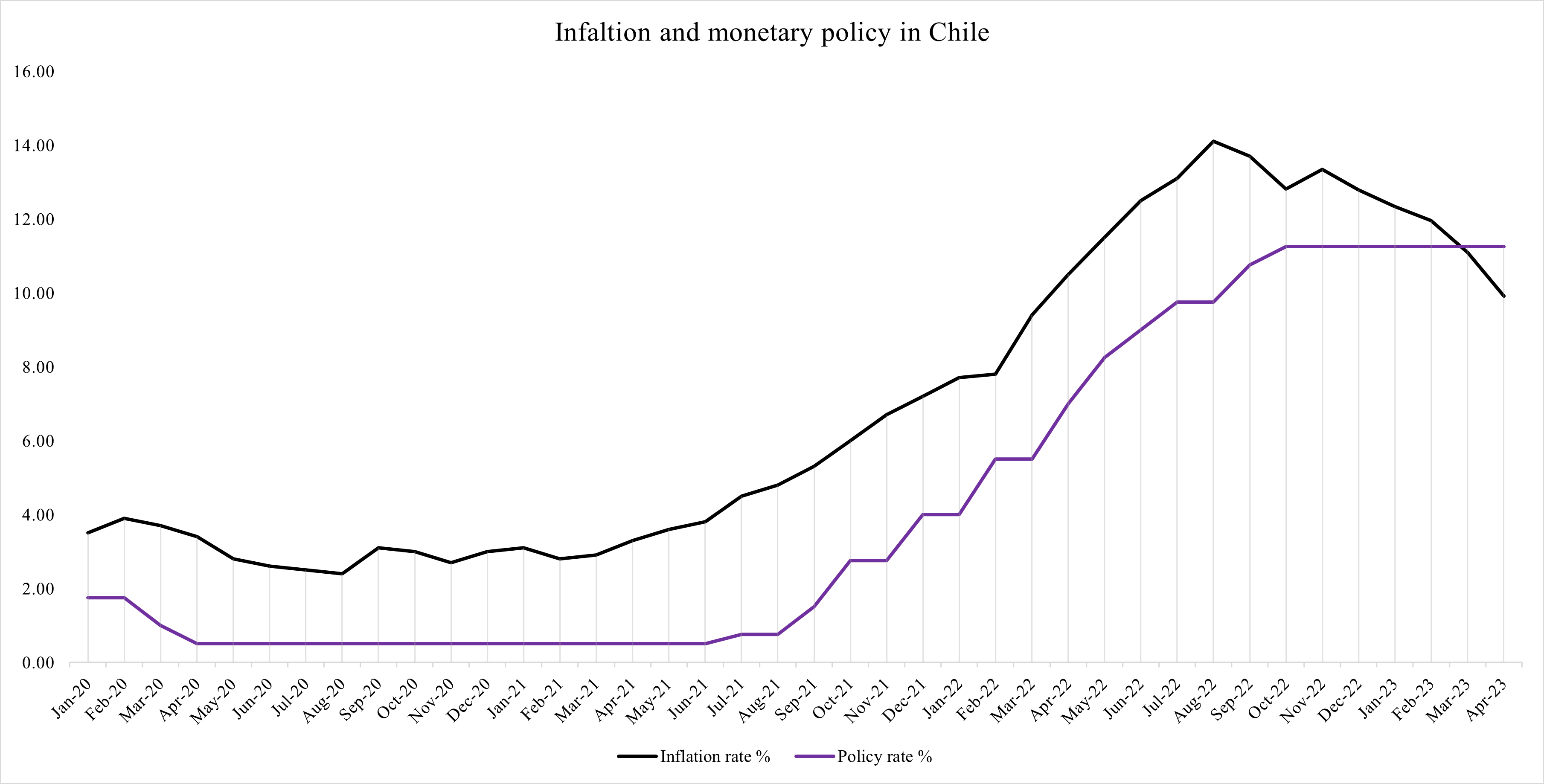

Chile central bank tightens credit conditions

On May 24th, Banco Central de Chile raised capital requirements on financial institutions, raising concerns over global risks. The measure tightens credit conditions; the central bank explained it was a “precautionary measure amid the higher global uncertainty”. According to central bank President Rosanna Costa, “this will have an insignificant impact on credit” and would only raise capital requirements by 0.5%. However, Chilean investment firm Vantrust Capital estimates that publicly-traded banks will have to create a $930mn buffer; Banco de Credito e Inversiones will have to set aside $300mn and Itaú Chile $165mn.

Expectations are growing that central bank policy will switch its target from bringing down inflation to encouraging growth. While high inflation is slowly falling, interest rates have been sustained at 11.25% since October 2022. Growth has slowed since mid-2021; for Q1 2023 it only grew by 0.8% from the prior three months, which is a 0.6% fall from a year before. Although Bloomberg calls this “bouncing back”, this half-growth is not sufficient to keep up with inflation and population growth alone. However, the finance ministry has raised its growth forecast to 0.3% from -0.7%, expecting higher copper prices – Chile’s main export – and more resilient domestic demand.

| A guest post by

|